What is Forward Volatility?

What is Forward Volatility?

Educational

Hi traders!

I'm here to chat a little about forward volatility.

When you're trading options, you want to look at the implied volatility (IV) of an option to gauge its price, rather than the dollar cost. This is because an IV value naturally accounts for different strikes and expiration dates, creating one commonly comparable value

Let's now discuss forward volatility, a concept that is similar to the "Forward Yield Curve" in bond trading.

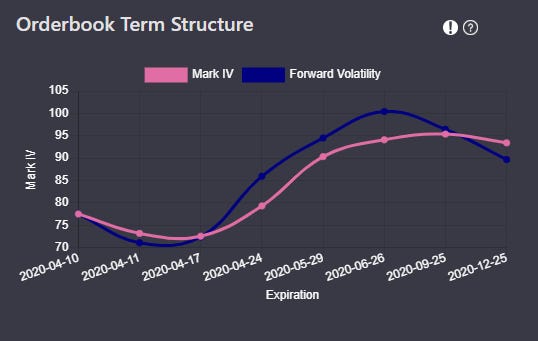

Pictured above, we have the At-The-Money BTC option term structure (pink). This gives us the ATM IV for each expiration cycle. This slope changes all the time.

In blue we have the Forward Volatility. This is the differential in IV between any two expiration cycles. Let's dig deeper.

June 26 has about 94.1% IV and 100.4% Forward-IV. What does Forward IV tell us?

Since May 29 IV is 90.33% but June 26 is 94.1% IV, the extra 27 days or so for June is really costing 100.4% IV. The extra 27 days have to be about 100.4% IV to lift the whole June 26 cycle IV to 94.1%...

Think about it like this.

From now until May 29th, IV is 90.33%

From 5/29 to 6/26 IV is 100.4%

Therefore, IV from now until 6/26 IV is 94.10%

This is forward IV, the differential IV between any two expiration cycles.

Using forward IV, a trader can gauge the most expensive portion of the term structure.

Here is the Math:

Forward IV = √[ (θ²T - σ²t) / (T -t)]

θ² = Longer dated option variance

σ² = Shorter dated option variance

T = time until expiration of longer dated option

t = time until expiration of shorter dated option

Hope this helps!

Follow us on twitter: https://twitter.com/GenesisVol

Disclaimer: Nothing here is a trade recommendation.

Trade at your own risk. Everything here is written for educational purposes only.

Everything is subject to typo's and other errors.

Use your best judgement.